Enterprise CRM Implementation: Breaking Free from the Platform Trap

Discover how NEO Home Loans breaks free from outdated CRMs by choosing scalable tech built for growth to empower top producers, unify data, and redefine ROI across the mortgage enterprise.

"Most companies end up trying to be everything for everyone – that system does not work," warns NEO Home Loans Co-Founder Ryan Grant. It's a trap that's ensnared countless mortgage organizations: fragmented technology stacks, siloed data, and a patchwork of solutions that create more problems than they solve.

But what separates organizations that successfully navigate enterprise technology adoption from those that get stuck in an endless cycle of implementations? I sat down with Grant to unpack the strategic frameworks that drive successful enterprise technology adoption in the mortgage industry.

The Platform Paradox

"The problem with most mortgage vendors, especially CRMs, is they were built on closed-end platforms with very limited abilities," Grant explains. This architectural limitation creates a costly cycle: companies implement solutions that work for current needs, but when requirements evolve, they struggle to keep up. "If something was outside of product scope or ability, you hit a brick wall. Then something else would come out, and you think 'I want that' – but your solution was built on a non-scalable platform” says Grant.

This pattern shines light onto why so many lenders find themselves constantly pursuing new solutions. It's not about feature lists or user interfaces – it's about core platform architecture that either enables or constrains future evolution.

Many mortgage professionals get trapped in an "originate, close, repeat" cycle that prevents true scaling: "When I was running a production team - as our volume would increase, I'd have to hire a new person to accommodate the increased business - but ultimately it wouldn't increase our bottom line. That's where a lot of people get stuck. They work very hard originating, but don't have the tools or right strategies to scale protitably".

Forward-thinking mortgage companies are addressing this by consolidating their tech stacks into unified platforms. This gives executives unprecedented visibility - from marketing campaign performance to branch profitability metrics and forecasting - while offering loan officers powerful tools that adapt to their workflows instead of forcing them into rigid processes, driving loan volume and performance.

Enterprise-Grade Evaluation

NEO's approach to technology evaluation cuts through traditional vendor selection processes, focusing on three critical areas often overlooked:

1. Architectural Flexibility

"Do your due diligence," Grant emphasizes. "Make sure the platform can evolve. The right platform is built to adapt with technology and scale as organizations evolve. Include AI portion of it can take things on – other CRMs weren't structured or engineered correctly from the beginning."

The key question: Can the platform adapt to emerging business models without requiring a complete overhaul?

2. Data Strategy Alignment

For NEO, technology must drive strategic value beyond basic automation. "We wanted to redefine our relationship with customers – we need value before, during, after," Grant explains.

"How do we add more value to our clients' lives. Emails with recipes is not valuable. We need a platform that analyzes data, is forward thinking, that helps us see and explore opportunities our clients may not see themselves."

3. Enterprise Performance Requirements

"What NEO needs is different," Grant notes. "If you need automation, data analytics, enterprise performance, tracking – you can get an off-the-shelf CRM that is good for an originator that is not good for an enterprise."

This distinction is critical.

Individual originators can get by with basic contact management and follow-up tools, but enterprise organizations require systems that deliver comprehensive visibility, enforce standardization where it matters, and scale effortlessly across branches, teams, and markets.

As Grant puts it, "We needed a platform that could handle the complexity of our operation while remaining simple enough for everyone to use effectively."

The 20% Factor & Why Top Producers Matter

Grant's experience reveals the reality of enterprise technology adoption: your top producers often drive innovation. "Higher level producers are inherently more creative, demanding, think outside the box, want things that standard CRM solutions can't do."

The challenge is balancing enterprise standardization with the needs of your most productive team members. But Grant has a solution for this.

"Knowing that you're not going to please everyone, you need a CRM that handles the core requirements for most users while offering enough flexibility for your power users to customize it to their specific workflows."

Proof that this works; "65% of our team has taken these tools and completely customized them to how they work with clients," says Grant. “Give talented people powerful, flexible tools, and they'll push the boundaries of what's possible.”

Many mortgage organizations fall into the trap of allowing multiple CRM systems to satisfy their top producers. Grant reveals why this is a strategic mistake: "I do not believe in the 'use whatever CRM you want' mentality – can't track, no scalability, no coaching. Most companies have to do that because they haven't invested in the tech that is best in class."

What does best-in-class tech actually look like?

Systems that bridge the gap between enterprise needs and individual users' preferences. A unified platform that integrates with your essential tools, offers functionality for multiple levels of users from novice loan officers to top producers, provides robust data analytics, and delivers the ease of use and support needed to drive successful company-wide adoption.

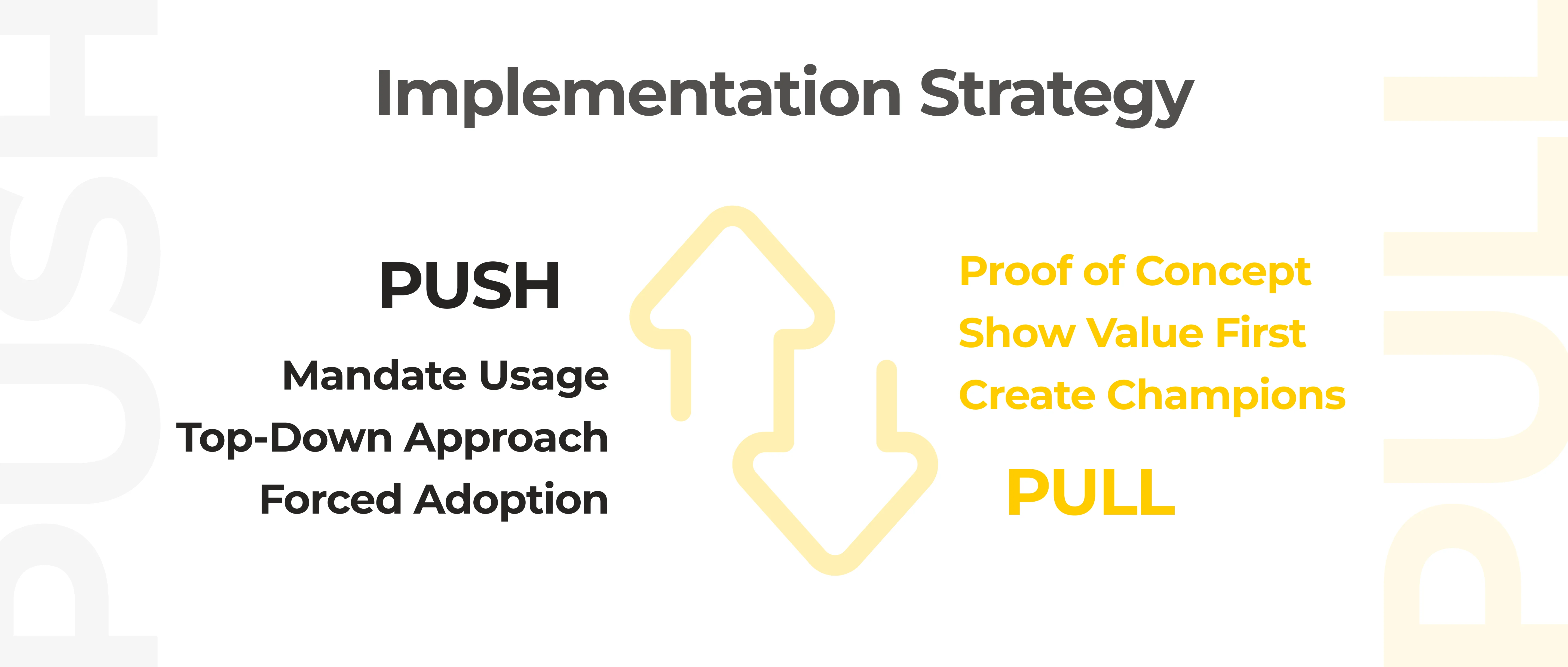

The Pull Method of Implementation

NEO's approach to technology adoption: Instead of mandating usage or pushing adoption from the top down, they've developed a "pull rather than push" strategy.

"Best thing we've done is proof of concept – what is a system doing that is helping others win. We will show you and pull you in, rather than pushing people in."

This approach creates internal champions who drive organic adoption throughout the organization. "We recruit that way," Grant explains. "This is the value you will get from it and that is how we will get better together."

By demonstrating value first, NEO addresses the most common hidden cost in technology implementation: lack of adoption. "If you pay for seats and execution/setup and no one uses it, then that was a waste," Grant points out.

This pull strategy relies on showcasing concrete results rather than just promising potential. When team members see industry peers increasing conversions through AI-powered lead prioritization, building tailored automations, or customizing their CRM to fit their workflow, they're naturally drawn to adopt the technology themselves.

Redefining ROI for Enterprise Technology

When evaluating technology investments, mortgage professionals often focus primarily on efficiency metrics and cost reduction. But Grant's experience points to a more comprehensive framework:

Looking Beyond Basic Automation

The real value of technology isn't just automating what you already do. Grant emphasizes looking at "what the system produces that the team couldn't produce on a different system."

His team discovered this firsthand: "When we first looked at the data, there was this small group – just 2% of our clients – that none of us had flagged as urgent. But the system showed they had over 40% purchase likelihood. We would've missed those opportunities for months."

These moments of insight – identifying opportunities that would otherwise remain invisible – represent value that standard ROI calculations simply can't capture.

Creating Strategic Advantages

Technology shouldn't just streamline operations – it should create new possibilities.

Grant notes that truly valuable technology fundamentally changes how a business operates: "We built such a great system that if we went to a different system it would jeopardize the success of my business." This perspective shifts ROI evaluation from just cost-reduction to deeply understanding how technology enables your team to do things they couldn't do before.

This level of strategic integration requires technology partners who work collaboratively with mortgage organizations to understand their unique workflows and objectives. Aidium's approach with customers like NEO exemplifies this partnership model – focusing on building systems that become essential to daily operations by continually adapting to evolving business needs rather than forcing organizations to conform to rigid software limitations.

Winning the Talent Game

In an industry where production is closely tied to individual performance, Grant suggests technology plays a crucial role in both attracting and retaining talent. He specifically points to "retention of your team" as a key ROI metric often overlooked in technology assessments.

For mortgage leaders, this means considering how technology choices affect your ability to recruit and keep top producers. Grant's approach of showing rather than telling – demonstrating technology value through proof of concept – becomes a powerful tool not just for internal adoption but also for attracting talent who want access to the best tools.

A New Approach to Mortgage Technology

The message from Grant's experience is clear: the future of mortgage technology is about making strategic choices that create a sustainable competitive advantage.

The mortgage organizations that will thrive are those that select platforms based on architectural flexibility rather than feature lists. They recognize that technology investments must align with their unique data strategy and enterprise requirements, not just satisfy the needs of a few.

Successful implementation requires balancing standardization with customization – providing a core platform that meets enterprise needs while giving top producers the flexibility to customize their workflows. When organizations invest in truly transformative technology and demonstrate its value, adoption follows naturally.

The mortgage industry has arrived at a crossroads. Organizations that continue chasing disconnected solutions will find themselves falling behind, while those that embrace modern platforms such as Aidium will create compounding advantages.

As markets and customer expectations evolve, the difference between leaders and followers won't just be the technology they choose, but how strategically they implement it. Breaking free from the platform trap isn't just about better technology – it's about building the foundation for sustained growth in an increasingly challenging landscape.

.svg)